In audit, it's essential to form an expectation of the Company's results before we really drill into the details. We compare the actual Company's results to our expectation, and investigate the variances accordingly. This is the analytical procedures adopted by most of the audit Company. Besides, we also compare the result / financial position with prior period.

Creditors' turnover anlaysis is one of the auditing procedure we performed. What are we expecting from the audit client, in general. We expect the creditors turnover (days) to increase, as compared to prior period.

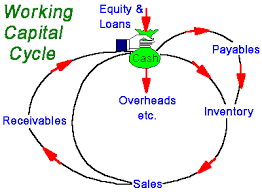

To illustrate, majority of our audit clients are affected by the economy turmoil. They are squeezing suppliers' credit ( by delyaing the repayment), in order to maintain the Company's working capital, as our audit client's working capital are most likely affected by the delay of repayment from customers.

We have formed an expectation, and we will compare the actual result with our expectation. Any unusual movements need to be identified.

Creditors' turnover anlaysis is one of the auditing procedure we performed. What are we expecting from the audit client, in general. We expect the creditors turnover (days) to increase, as compared to prior period.

To illustrate, majority of our audit clients are affected by the economy turmoil. They are squeezing suppliers' credit ( by delyaing the repayment), in order to maintain the Company's working capital, as our audit client's working capital are most likely affected by the delay of repayment from customers.

We have formed an expectation, and we will compare the actual result with our expectation. Any unusual movements need to be identified.

No comments:

Post a Comment