Advertising is a strong mediun to promote business.It is a form of communication intended to persuade an audience (viewers, readers or listeners) to purchase or take some action upon products, ideas, or services. It includes the name of a product or service and how that product or service could benefit the consumer, to persuade a target market to purchase or to consume that particular brand. These messages are usually paid for by sponsors and viewed via various media. Advertising can also serve to communicate an idea to a large number of people in an attempt to convince them to take a certain action.Commercial advertisers often seek to generate increased consumption of their products or services through branding, which involves the repetition of an image or product name in an effort to associate related qualities with the brand in the minds of consumers. Non-commercial advertisers who spend money to advertise items other than a consumer product or service include political parties, interest groups, religious organizations and governmental agencies. Nonprofit organizations may rely on free modes of persuasion, such as a public service announcement.Virtually any medium can be used for advertising. Commercial advertising media can include wall paintings, billboards, street furniture components, printed flyers and rack cards, radio, cinema and television adverts, web banners, mobile telephone screens, shopping carts, web popups, skywriting, bus stop benches, human billboards, magazines, newspapers, town criers, sides of buses, banners attached to or sides of airplanes ("logojets"), in-flight advertisements on seatback tray tables or overhead storage bins, taxicab doors, roof mounts and passenger screens, musical stage shows, subway platforms and trains, elastic bands on disposable diapers,doors of bathroom stalls,stickers on apples in supermarkets, shopping cart handles (grabertising), the opening section of streaming audio and video, posters, and the backs of event tickets and supermarket receipts. Any place an "identified" sponsor pays to deliver their message through a medium is advertising.Virtually any medium can be used for advertising. Commercial advertising media can include wall paintings, billboards, street furniture components, printed flyers and rack cards, radio, cinema and television adverts, web banners, mobile telephone screens, shopping carts, web popups, skywriting, bus stop benches, human billboards, magazines, newspapers, town criers, sides of buses, banners attached to or sides of airplanes ("logojets"), in-flight advertisements on seatback tray tables or overhead storage bins, taxicab doors, roof mounts and passenger screens, musical stage shows, subway platforms and trains, elastic bands on disposable diapers,doors of bathroom stalls,stickers on apples in supermarkets, shopping cart handles (grabertising), the opening section of streaming audio and video, posters, and the backs of event tickets and supermarket receipts. Any place an "identified" sponsor pays to deliver their message through a medium is advertising.

Advertising is a strong mediun to promote business.It is a form of communication intended to persuade an audience (viewers, readers or listeners) to purchase or take some action upon products, ideas, or services. It includes the name of a product or service and how that product or service could benefit the consumer, to persuade a target market to purchase or to consume that particular brand. These messages are usually paid for by sponsors and viewed via various media. Advertising can also serve to communicate an idea to a large number of people in an attempt to convince them to take a certain action.Commercial advertisers often seek to generate increased consumption of their products or services through branding, which involves the repetition of an image or product name in an effort to associate related qualities with the brand in the minds of consumers. Non-commercial advertisers who spend money to advertise items other than a consumer product or service include political parties, interest groups, religious organizations and governmental agencies. Nonprofit organizations may rely on free modes of persuasion, such as a public service announcement.Virtually any medium can be used for advertising. Commercial advertising media can include wall paintings, billboards, street furniture components, printed flyers and rack cards, radio, cinema and television adverts, web banners, mobile telephone screens, shopping carts, web popups, skywriting, bus stop benches, human billboards, magazines, newspapers, town criers, sides of buses, banners attached to or sides of airplanes ("logojets"), in-flight advertisements on seatback tray tables or overhead storage bins, taxicab doors, roof mounts and passenger screens, musical stage shows, subway platforms and trains, elastic bands on disposable diapers,doors of bathroom stalls,stickers on apples in supermarkets, shopping cart handles (grabertising), the opening section of streaming audio and video, posters, and the backs of event tickets and supermarket receipts. Any place an "identified" sponsor pays to deliver their message through a medium is advertising.Virtually any medium can be used for advertising. Commercial advertising media can include wall paintings, billboards, street furniture components, printed flyers and rack cards, radio, cinema and television adverts, web banners, mobile telephone screens, shopping carts, web popups, skywriting, bus stop benches, human billboards, magazines, newspapers, town criers, sides of buses, banners attached to or sides of airplanes ("logojets"), in-flight advertisements on seatback tray tables or overhead storage bins, taxicab doors, roof mounts and passenger screens, musical stage shows, subway platforms and trains, elastic bands on disposable diapers,doors of bathroom stalls,stickers on apples in supermarkets, shopping cart handles (grabertising), the opening section of streaming audio and video, posters, and the backs of event tickets and supermarket receipts. Any place an "identified" sponsor pays to deliver their message through a medium is advertising.Tuesday, November 30, 2010

Advertising

Advertising is a strong mediun to promote business.It is a form of communication intended to persuade an audience (viewers, readers or listeners) to purchase or take some action upon products, ideas, or services. It includes the name of a product or service and how that product or service could benefit the consumer, to persuade a target market to purchase or to consume that particular brand. These messages are usually paid for by sponsors and viewed via various media. Advertising can also serve to communicate an idea to a large number of people in an attempt to convince them to take a certain action.Commercial advertisers often seek to generate increased consumption of their products or services through branding, which involves the repetition of an image or product name in an effort to associate related qualities with the brand in the minds of consumers. Non-commercial advertisers who spend money to advertise items other than a consumer product or service include political parties, interest groups, religious organizations and governmental agencies. Nonprofit organizations may rely on free modes of persuasion, such as a public service announcement.Virtually any medium can be used for advertising. Commercial advertising media can include wall paintings, billboards, street furniture components, printed flyers and rack cards, radio, cinema and television adverts, web banners, mobile telephone screens, shopping carts, web popups, skywriting, bus stop benches, human billboards, magazines, newspapers, town criers, sides of buses, banners attached to or sides of airplanes ("logojets"), in-flight advertisements on seatback tray tables or overhead storage bins, taxicab doors, roof mounts and passenger screens, musical stage shows, subway platforms and trains, elastic bands on disposable diapers,doors of bathroom stalls,stickers on apples in supermarkets, shopping cart handles (grabertising), the opening section of streaming audio and video, posters, and the backs of event tickets and supermarket receipts. Any place an "identified" sponsor pays to deliver their message through a medium is advertising.Virtually any medium can be used for advertising. Commercial advertising media can include wall paintings, billboards, street furniture components, printed flyers and rack cards, radio, cinema and television adverts, web banners, mobile telephone screens, shopping carts, web popups, skywriting, bus stop benches, human billboards, magazines, newspapers, town criers, sides of buses, banners attached to or sides of airplanes ("logojets"), in-flight advertisements on seatback tray tables or overhead storage bins, taxicab doors, roof mounts and passenger screens, musical stage shows, subway platforms and trains, elastic bands on disposable diapers,doors of bathroom stalls,stickers on apples in supermarkets, shopping cart handles (grabertising), the opening section of streaming audio and video, posters, and the backs of event tickets and supermarket receipts. Any place an "identified" sponsor pays to deliver their message through a medium is advertising.Monday, November 29, 2010

Business Plans

When we thinking of starting a business we should put a plan .Writing a plan is not a difficult task and the process we have put together will help both we and our business get off to the best start possible with confidence.We need a good plan to run the business.If we never written a business plan before the whole process can feel daunting when it comes to financial projections and marketing.That's why we have developed a range of ready made business plans that already have all the required sections already completed so all we need do is customize the plan for your own business.

When we thinking of starting a business we should put a plan .Writing a plan is not a difficult task and the process we have put together will help both we and our business get off to the best start possible with confidence.We need a good plan to run the business.If we never written a business plan before the whole process can feel daunting when it comes to financial projections and marketing.That's why we have developed a range of ready made business plans that already have all the required sections already completed so all we need do is customize the plan for your own business.In 2001 Turmeric Business Plans have sold over 43,000 plans in the UK and worldwide. These plans and our consulting service are guaranteed to get you band finance or we refund your purchase. So whether you download a sample business plan or get us to write a business plan for your start up business you can be rest assured that you have the best resources to hand.Once your purchase has been confirmed you"ll get access to your own personal download page where you can view or download your product to your computer. Our plans are written in Microsoft Word and the financial forecasts in Microsoft Excel which are easy programs to use.You'll get unlimited access to your business plan and other related business tools for a whole 12 months for one the financial forecasts in Microsoft Excel which are easy programs to use.

Sunday, November 28, 2010

Types of Business

There are many types of business.A business also known as company, enterprise or firm is a legally recognized organization designed to provide goods, services or both to consumes or tertiary business in exchange money.The business are predominant in capitalist economies, in which most business are privately owned and typically formed to earn profit that will increase the wealth and typically formed to earn profit that will increase the wealth of its owner. The main objectives of business is the receip or generation of a financial return in exchange for work and acceptance of risk. Business can also be formed not for profit or be state owned.

There are many types of business.A business also known as company, enterprise or firm is a legally recognized organization designed to provide goods, services or both to consumes or tertiary business in exchange money.The business are predominant in capitalist economies, in which most business are privately owned and typically formed to earn profit that will increase the wealth and typically formed to earn profit that will increase the wealth of its owner. The main objectives of business is the receip or generation of a financial return in exchange for work and acceptance of risk. Business can also be formed not for profit or be state owned.There are several common forms of business:Sole proprietorship: It is a business for profit owned by one person. the owner may operate on his or her own or may employ others. The owner of the business has unlimited liability for the debts incurred by the business.

Partnership: A form of for profit business owned by two or more people. In partnership business each partner has unlimited liability for the debts incurred by the business.

Corporation: Can be either or private in nature. A public company is often listed of the stock exchange and typically has unlimited liability.Privately owned companies have limited liability and are often signified by the term "Pvt. Ltd".

Cooperative: Often referred to as a "co-op", a cooperative is a limited liability entity that can be organized for profit or not for profit.Cooperatives are typically classified as either consumer cooperatives or worker cooperatives. Cooperatives are fundamental to the ideology of economic democracy.

Cooperative: Often referred to as a "co-op", a cooperative is a limited liability entity that can be organized for profit or not for profit.Cooperatives are typically classified as either consumer cooperatives or worker cooperatives. Cooperatives are fundamental to the ideology of economic democracy.

Saturday, November 20, 2010

Accounting principle- Accrual Basis

Figures generated / kept in accordance to accounting principle is prepared on accrual basis. For instance, accountant record the provision for warranty ( based on estimate) even though there's no actual cash/ economic outflow yet.

In finance, cash basis figures are more relatively more valuable , as compared to accrual basis ( advocated by accounting principle), in order to value a business.

What do you think ? You prefer a an accrual method or cash method in valuing a business?

In finance, cash basis figures are more relatively more valuable , as compared to accrual basis ( advocated by accounting principle), in order to value a business.

What do you think ? You prefer a an accrual method or cash method in valuing a business?

Auditing Creditors- Creditor Turnover Analysis

In audit, it's essential to form an expectation of the Company's results before we really drill into the details. We compare the actual Company's results to our expectation, and investigate the variances accordingly. This is the analytical procedures adopted by most of the audit Company. Besides, we also compare the result / financial position with prior period.

Creditors' turnover anlaysis is one of the auditing procedure we performed. What are we expecting from the audit client, in general. We expect the creditors turnover (days) to increase, as compared to prior period.

To illustrate, majority of our audit clients are affected by the economy turmoil. They are squeezing suppliers' credit ( by delyaing the repayment), in order to maintain the Company's working capital, as our audit client's working capital are most likely affected by the delay of repayment from customers.

We have formed an expectation, and we will compare the actual result with our expectation. Any unusual movements need to be identified.

Creditors' turnover anlaysis is one of the auditing procedure we performed. What are we expecting from the audit client, in general. We expect the creditors turnover (days) to increase, as compared to prior period.

To illustrate, majority of our audit clients are affected by the economy turmoil. They are squeezing suppliers' credit ( by delyaing the repayment), in order to maintain the Company's working capital, as our audit client's working capital are most likely affected by the delay of repayment from customers.

We have formed an expectation, and we will compare the actual result with our expectation. Any unusual movements need to be identified.

Auditing: Annual Budget vs Actual Results

Company prepare budget and use budget as a performance benchmark and monitoring tools. For instance, senior management can question sales department if their actual yeat-to-date entertainment has exceeded the budget before the end of the year. Budget is , usually, prepared and approved at the beginning of the year or before that.

Budget has incorporated management's forecast, estimation and outlook of the business in the coming times.

Is management's budget useful to auditor?

The answer is yes. Budget, which represents management's expectation, should be compared against the actual results. Significant variances should be investigated. Apparently, management would have to explain the variances. It's important for auditor to find out the reason of the variances to identify potential changes in business operation, significant developments during the year.

Understanding how management view the business (by looking at the budget) is a crucial stage in audit planning, it enhance our knowledge and understanding on the business, the industry and the overall economy as a whole.

Budget has incorporated management's forecast, estimation and outlook of the business in the coming times.

Is management's budget useful to auditor?

The answer is yes. Budget, which represents management's expectation, should be compared against the actual results. Significant variances should be investigated. Apparently, management would have to explain the variances. It's important for auditor to find out the reason of the variances to identify potential changes in business operation, significant developments during the year.

Understanding how management view the business (by looking at the budget) is a crucial stage in audit planning, it enhance our knowledge and understanding on the business, the industry and the overall economy as a whole.

Disposing capital-intensive business

What's happening in the corporate world now?

Capital-intensive require heavy investment of resources, including, but not limimted to: cash, human resource,management's effort, etc. As part of the restructuring exercise to scale down, there are evidence that a lot of corporate are disposing off capital-intensive business.

How would disposing capital-intensive business benefit the corporate?

- immediate liquidity ( i.e. proceeds from disposal)

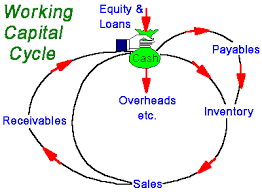

- better working capital management

- allow management to evaluate other business opportunities

- lesser resources are required, which allow the business to scale down

- higher return on asset ("ROA") ratio

However, it's always not easy to dispose off a capital-intensive business unit/ busines during this business environment, unless a substantial discount is given to the potential buyers.

Capital-intensive require heavy investment of resources, including, but not limimted to: cash, human resource,management's effort, etc. As part of the restructuring exercise to scale down, there are evidence that a lot of corporate are disposing off capital-intensive business.

How would disposing capital-intensive business benefit the corporate?

- immediate liquidity ( i.e. proceeds from disposal)

- better working capital management

- allow management to evaluate other business opportunities

- lesser resources are required, which allow the business to scale down

- higher return on asset ("ROA") ratio

However, it's always not easy to dispose off a capital-intensive business unit/ busines during this business environment, unless a substantial discount is given to the potential buyers.

Accounting treatment for tax penalty

One of our Accounting & Audiitng blog reader inquired us the following:

" How should penalty on late repayment for tax been accounted for?"

Should it be a tax expense? Should it be other expenses?

To clarify: penalty imposed by inland revenue authority on late repayment for tax should not be accounted for as tax expense; it should be accounted for as administrative expense/ other expense.

" How should penalty on late repayment for tax been accounted for?"

Should it be a tax expense? Should it be other expenses?

To clarify: penalty imposed by inland revenue authority on late repayment for tax should not be accounted for as tax expense; it should be accounted for as administrative expense/ other expense.

No depreciation charge on asset held for sale

This is to confirm that if a property is classified as asset held for sale, no depreciation is to be recorded.

To illustrate, Company ABC entered into Sales & Purchase agreement with 3rd party to dispose one of its property. The Sales & Purchase agreement may take months to complete. In this instance, Company ABC re-classified the property from Property, Plant & Equipment to Asset held for Sale upon entering the Sales & Purchase agreement.

Asset held for sale is de-recognised from the balance sheet upon the completion of the Sales & Purchase agreement.

To illustrate, Company ABC entered into Sales & Purchase agreement with 3rd party to dispose one of its property. The Sales & Purchase agreement may take months to complete. In this instance, Company ABC re-classified the property from Property, Plant & Equipment to Asset held for Sale upon entering the Sales & Purchase agreement.

Asset held for sale is de-recognised from the balance sheet upon the completion of the Sales & Purchase agreement.

Auditing Creditors

One of the procedures required to audit trade creditors account is to audit the creditors' statement received from the audit client's suppliers (i.e. external audit evidence).

In normal business circumstances, suppliers will send their monthly Statement of Account to their customers to inform the customers in relation to the outstanding balances. Hence, our audit client will , most likely, receive statement of account from the suppliers.

As part of audit procedure, we can check the suppliers' statement (received by our audit customers) against the creditors' balance recorded in their book. Discrepancies need to be investigated. Statement of account served as an external confirmation to check if our audit client's book has been prepared properly.

However, there are suppliers who do not have practices of sending out Statement of Account to their customers. In this instance, we can send external audit confirmation to the suppliers to confirm outstanding balances.

In normal business circumstances, suppliers will send their monthly Statement of Account to their customers to inform the customers in relation to the outstanding balances. Hence, our audit client will , most likely, receive statement of account from the suppliers.

As part of audit procedure, we can check the suppliers' statement (received by our audit customers) against the creditors' balance recorded in their book. Discrepancies need to be investigated. Statement of account served as an external confirmation to check if our audit client's book has been prepared properly.

However, there are suppliers who do not have practices of sending out Statement of Account to their customers. In this instance, we can send external audit confirmation to the suppliers to confirm outstanding balances.

Cash audit- internal controls in cash process- cash payment

In our earlies entries in relation to cash audit, we discussed about the audit procedures of auditing unpresented cheques. We will discuss more extensively for audit procedures in auditing cash and bank balances of our audit clients.

Auditors may consider test the internal controls of the client's cash process. For this entry, we will provide an overview of the possible audit procedures to test the internal controls in cash payment process:

(a) select certain number of random samples, and test that payment voucher are properly prepared and authorised

(b) select certain number of random samples, and test that bank reconciliations are properly prepared and reviewed

(c) select certain number of random samples, and test that journal entries are properly posted into General Ledger

(d) select certain number of random samples, and test that payment voucher details match with the corresponding payment details

Auditors may consider test the internal controls of the client's cash process. For this entry, we will provide an overview of the possible audit procedures to test the internal controls in cash payment process:

(a) select certain number of random samples, and test that payment voucher are properly prepared and authorised

(b) select certain number of random samples, and test that bank reconciliations are properly prepared and reviewed

(c) select certain number of random samples, and test that journal entries are properly posted into General Ledger

(d) select certain number of random samples, and test that payment voucher details match with the corresponding payment details

Thursday, November 11, 2010

The Types Of Accounting

Accounting is the art of analyzing and interpreting data. It may not be apparent to some but every business and every individual uses accounting in some form. An individual may knowingly or unknowingly use accounting when he evaluates his financial information and relays the results to others. Accounting is an indispensable tool in any business, may it be small or multi-national.

The term "accounting" covers many different types of accounting on the basis of the group or groups served. The following are the types of accounting.

1. Private or Industrial Accounting: This type of accounting refers to accounting activity that is limited only to a single firm. A private accountant provides his skills and services to a single employer and receives salary on an employer-employee basis. The term private is applied to the accountant and the accounting service he renders. The term is used when an employer-employee type of relationship exists even though the employer is some case is a public corporation.

2. Public Accounting: Public accounting refers to the accounting service offered by a public accountant to the general public. When a practitioner-client relationship exists, the accountant is referred to as a public accountant. Public accounting is considered to be more professional than private accounting. Both certified and non certified public accountants can provide public accounting services. Certified accountants can be single practitioners or by partnership ranging in size from two to hundreds of members. The scope of these accounting firms can include local, national and international clientele.

3. Governmental Accounting: Governmental accounting refers to accounting for a branch or unit of government at any level, may it be federal, state, or local. Governmental accounting is very similar to conventional accounting methods. Both the governmental and conventional accounting methods use the double-entry system of accounting and journals and ledgers. The object of government accounting units is to give service rather than make profits. Since profit motive cannot be used as a measure of efficiency in government units, other control measures must be developed. To enhance control, special funds accounting is used. Governmental units can use the services of both private and public accountant just as any business entity.

4. Fiduciary Accounting: Fiduciary accounting lies in the notion of trust. This type of accounting is done by a trustee, administrator, executor, or anyone in a position of trust. His work is to keep the records and prepares the reports. This may be authorized by or under the jurisdiction of a court of law. The fiduciary accountant should seek out and control all property subject to the estate or trust. The concept of proprietorship that is common in the usual types of accounting is non-existent or greatly modified in fiduciary accounting.

5. National Income Accounting: National income accounting uses the economic or social concept in establishing accounting rather than the usual business entity concept. The national income accounting is responsible in providing the public an estimate of the nation's annual purchasing power. The GNP or the gross national product is a related term, which refers to the total market value of all the goods and services produced by a country within a given period of time, usually a calendar year.

Should I Practice Public Or Private Accounting

Bachelor of Science in Accountancy is one of the picked courses among college students. Many have chosen this field of study because it has a wide scope of availability in terms of future stable job with attach high rate of pay. Career opportunities in this course have two categories and these are Public and Private Accounting.

Professionals who worked for a particular Accounting Firm and worked for several clients are called Public Accountants. These kind of firms employ thousands of accountants because their services are offered from one-person operations to multinational organizations. Audit or tax is two paths where in a Public accountant is going to be. Auditors as you called for those in the audit practice strictly and carefully audit financial records and business transactions of a client. Accounting records that are reported by the companies are ensured by the auditors that those documents accurately abide with national accounting standards. Professionals who are in the tax practice provide services similar with that of an auditor but with a more focus specialization. Professionals who handles tax ensures that clients tax record are well documented and do follow the guidelines established by government taxing policies. Another role of a tax accountant is to help minimize the tax liability of a client.

On the other hand Private Accounting is more concern with internal accounting. This internal accounting is the accounting functions of the company. Corporate Accountants which is another name for private accountant performs the same duties as the Public accountant but this task are limited towards the companies that they are employed.

The distinction between Public and private Accounting is that Public is more involved with collecting external financial information's while Private is much inclined with the use of internal information's to aid managers in giving effective decisions.

Questions and Answers About Starting an Accounting Career

An accountant plays a very important role in the functioning and efficiency of a corporation. They provide a number of vital business services to clients including the management of financial matters, auditing, and handling tax issues. However, the specific duties performed in an accounting career will differ depending on what field the practitioner works in, be it public accounting, management accounting, government accounting, or internal auditing.

Accountants will generally use computers and special accounting programs to assist them in their duties. Accountants can summarize and organize data in particular formats to make them more suitable for storage or analysis. The programs also remove a lot of the tedious manual work of accounting out of the job. For this reason, accountants will generally have a very high level of competence with computers and many employers will require them to be proficient in these programs to help keep their work accurate.

The environment in which an accountant works will generally vary depending on what field of accounting he/she is in as well as what type of company or organization he/she works for. The vast majority of accountants work in an office setting, often with many other coworkers and colleagues; although, some accountants are self-employed and may be able to work part of their job at home as well. Most accountants work a standard 40-hour week; though, there are exceptions especially in the case of tax specialists and self-employed accountants who may work longer hours during certain times of the year.

Public accounting firms often send their accountants to their clients' place of work or residence to perform audits. In this scenario, there can also be a lot of traveling involved. Accountants who travel often will most likely use a laptop to allow for the increased mobility of their accounting programs, data, and other information needed on the job.

Accountants, regardless of their chosen field, require a proficiency in mathematics as well as business. Many accountants are unlicensed, especially in the fields of government accounting, management accounting, and internal auditing. A bachelor's degree in accounting or a related field is required to become licensed as a Certified Public Accountant (CPA), Public Accountant (PA), Registered Public Accountant (RPA), or Accounting Practitioner (AP). Some companies will require their accountants to hold master's degrees as well.

There is a large demand for accountants, and as more businesses are created in the coming years, the demand is expected to increase. The rapid expansion of business is also expected to have a large effect on the types of responsibilities accountants will have. Nevertheless, these jobs can be very competitive, and many businesses are increasing their standards by which they hire and the qualifications they demand.

Accountants who have a great knowledge of computers and many different accounting software will have a better change of employment. Also, those who have more education, training, and experience will also have an edge in the job market. It is also important for accountants to demonstrate interpersonal skills as this will also help them perform their job more effectively and get along better with clients.

Find the Right Type of Accountant to Hire

In today's world of regulated business, there is increasing pressure on companies to have transparency in their financial statements. This push from shareholders and government agencies has caused a large increase in the need for external accounting, transforming audit and tax services into a commodity. The fact that these firms are now so popular means they will offer you many discounts and incentives to obtain your business as a client. In order to obtain the correct firm, it is important to know what type of service professional you need.

First, you need to prioritize the main reason in reaching out to a professional. If you are looking specifically for help with taxes or tax planning there are many small firms available to assist your business. Many of these firms can be franchises such as H&R Block or LedgerPlus or they can also be local private firms. Before committing, it is important to look at the tax firm's employees. Many will have what is called an EA, or enrolled agent. These are licensed tax professionals who are certified by the IRS after taking a test covering all types of business taxes from public to private. This type of professional will be able to do sufficient work for a small business and can be significantly cheaper than hiring a larger or public accounting firm.

If your company is in need of an audit for shareholders, or you are a private firm looking for a professional audit, it is a good idea to go with a public accounting firm. These large firms consist of Certified Public Accountants, or CPAs. CPAs are held to the highest standards by the PCAOB and have to pass a rigorous test and continue education throughout their career. Although public firms will bill you more, they hold themselves to a much higher standard for quality of work. Also, public accounting firms will do a preliminary audit of your business before they decide to take on your company as a client. This is to make sure they do not see any red flags or feel that they could give your company an adverse opinion.

Because of this, you can trust these public firms more being that they do not want to be liable for assuring your financial statements if it later comes out your company has committed fraud. Another bonus of a public firm is their representation if there is ever any litigation against your business. Many times upset shareholders want to sue a publicly traded company because they lost their investment based on so called misleading financial statements. In this case the accounting firm will stand up for you in court and defend your numbers against the prosecuting party.

These are just two basic reasons to choose an accounting firm to help your business. It is very important to evaluate your individual situation before deciding on a specific accounting professional.

Subscribe to:

Comments (Atom)